The thread between this week's IPO filings and the SEC's accredited investor amendments

The thread between this week's IPO filings and the SEC's accredited investor amendments

Plus, more M&A in video conferencing

What’s The Deal is a free newsletter that analyzes the biggest stories, and profiles important players, in Venture Capital, Private Equity, and Financial Markets.

Here’s a pop quiz question for readers: What do the companies that filed to go public this week have in common?

One correct (albeit obvious) answer is they’re all technology firms. Asana is a productivity software tool, Snowflake provides data storage, Palantir offers data analytics, Unity is a gaming platform, JFrog is used by software developers, and Sumo Logic provides cloud data analytics. With technology stocks soaring amid (because of?) the pandemic, it’s no surprise that well-funded tech startups and their VC backers are eager to tap into public market enthusiasm.

A second correct answer would be they’re all unprofitable or barely profitable. In the last fiscal year, Asana lost $118.6 million (more than double its previous year’s losses), Snowflake lost $348.5 million (nearly double last year’s losses), Palantir lost a whopping $580 million (almost the exact same it lost last year), Unity lost $163.2 million (a hair greater than its 2018 losses), Sumo Logic lost $92.1 million (almost double last year’s), and JFrog lost $5.4 million (although JFrog turned a profit last quarter).

To be fair to these companies: (1) Their revenue, like their losses, are growing, meaning the companies are on track to achieving profitability one day, and (2) Going public while being unprofitable is par for the course: just 24% of companies that went public in 2019 reported positive net income, the lowest level since 2001’s dot-com bubble, according to Goldman Sachs.

But it’s not just under-the-radar technology companies that are losing money when going public. Ride-sharing platforms Uber and Lyft reported losses of $1.8 billion and $900 million respectively ahead of their 2019 IPOs. Home-sharing giant Airbnb, which now plans to go public in 2020, was profitable in 2018 but unprofitable in 2019, even as its revenue increased. As I wrote in the spring:

[In 2019] Airbnb increased its marketing budget by 58%. It purchased another company for $400 million in cash and stock. It sank money into its Experiences product. In effect, Airbnb deliberately transformed itself into a loss-making company to get more customers and contractors (“hosts”) onto its platform, diversify its revenue, and build hype for its IPO.

The practice of companies “deliberately” sustaining losses pre-IPO is the entire point here. Executives, investors, managerial employees – those responsible for whether a company is profitable or not – are not directly impacted by whether a company sustains losses, so long as it continues growing. But these equity-holding stakeholders are directly impacted by the company’s valuation, which is more closely tied to customer and revenue growth. To put it plainly: a company’s leaders face little incentive to focus on profitability and a lot of incentive to focus on top-line growth.

The question is, who eats a private company’s pre-IPO losses?

That depends on the fate of the company. If a startup is unable to continue growing and shuts down, then its VC investors are the ones who lose money (and by extension, retail investors don’t get burned). But, according to critics, if an unprofitable startup is successful and eventually IPOs, then mom-and-pop investors – those restricted to investing in public markets – are left stomaching the company’s losses, in the sense that they cannot profit from that company’s pre-IPO valuation hikes, and that the listing value of public shares is grossly inflated, and only made possible by that company’s net losses.

Which brings us to yesterday’s announcement from The Securities and Exchange Commission that it has expanded its definition of “accredited investors” (those allowed to invest in private shares) to include holders of entry-level stockbroker’s licenses and employees of private firms. Perhaps most consequentially, the SEC also says it is opening the door to expanding further its “accredited investor” definition in the future. (As I wrote last month, the Trump administration has been engaged in a years-long campaign to lower the barriers to entry for private markets, which includes a DOL initiative to allow 401ks to invest in PE funds).

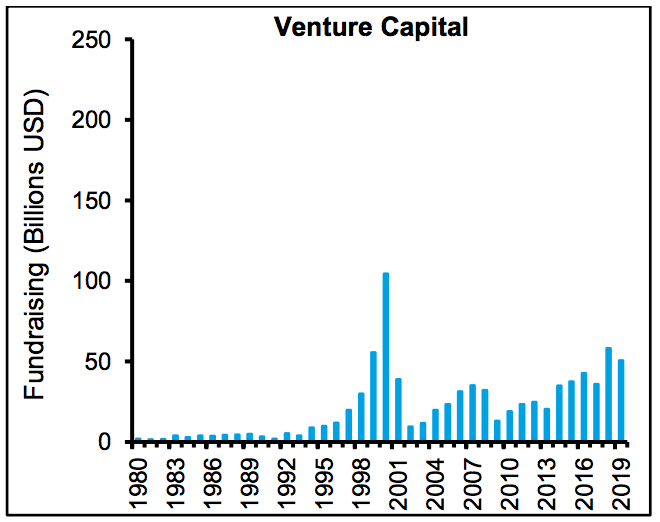

The growth of Venture Capital funding reflects the economy’s increase in private market activity (Source: Morgan Stanley).

In effect, the SEC’s order means that more individual investors can participate in funding rounds of private companies, like those that filed to go public this week. Hypothetically, this means that more investors can capture the value that startups accrue during their early stages of pre-IPO growth. (It also means that more individuals can now invest in hedge funds and leveraged-buyout firms, the implications of which we’ll leave for another day).

It’s worth considering what exactly the SEC’s goal is. If it’s to truly reduce inequality in the financial system, then other remedies are called for: stockbrokers and PE firm employees are already in the top 1-2% of income and wealth strata; they aren’t going hungry without access to private markets. But if the goal is to make rich people richer (and to give them more freedom of choice in their investing), then the SEC will likely succeed (at least partially), since more financial professionals will start investing in startups, and some of them will do very well. Of course, some of them will do very poorly, but the good news is they’re already comfortable, so they can stomach the losses.

Perhaps the most impactful long-term consequence here is simply ushering more money into private markets, which could increase competition for funding deals and accelerate the long-term shift of capital from public to private markets. In a world where there are more private market investors, private companies are likely to stay private longer, which could make public markets even less profitable to ordinary people and their 401ks.

One thing here is certain: The growth of private market activity isn’t slowing down, and it will continue to transform the economy, businesses, and our financial system.

If you’re enjoying What’s The Deal, don’t forget to subscribe!

“Work is what you do, not where you go. With this reality, unwanted background noise has become one of the most common and frustrating distractions in today’s work environment.” - Cisco on its acquisition of AI startup BabbleLabs

M&A in the booming video conferencing space is gaining momentum.

This week’s announcement that Cisco is acquiring BabbleLabs, a startup that uses “advanced AI techniques to distinguish human speech from unwanted noise, enhancing the quality of communications and conferencing applications,” comes on the heels of similar deals.

Back in May, market leader Zoom acquired its first company, Keybase, a 25-person start-up that would help Zoom add end-to-end encryption to video calls. The deal took place just as Zoom was experiencing its first major PR challenge, as so-called “Zoom Bombers” interrupted school sessions, church meetings, and all the other formerly face-to-face interactions now happening online due to the pandemic.

Also in May, telecommunications giant Verizon completed a $500 million deal for videoconferencing company Blue Jeans. TechCrunch reported the deal was “about much more than the short-term requirements of COVID-19” and that Verizon “saw an enterprise-grade video conferencing platform that would fit nicely into its 5G strategy around things like telemedicine and online learning.”

Bottom-line: Whether or not the pandemic portends the “death of the office”, one trend is clear: More people will work and socialize remotely in the future than in the past, which means video conferencing has a long runway ahead of it. Look for more M&A in the months ahead, particularly as tech giants like Google and Facebook seek to bolster their own products.

Private Equity

“Buyout groups team up in €13bn battle for Italy’s Serie A: Private equity groups CVC Capital Partners and Advent International have teamed up for a €1.3bn bid to acquire a minority stake in Italy’s Serie A football competition, as clubs near a decision on whether to bring outside investors into one of Europe’s biggest leagues.” (FT)

“TPG Planning Two Blank-Check IPOs Amid SPAC Boom: Private equity firm TPG is preparing to raise around $700 million via two blank-check companies that would add to this year’s already record tally for such deals, according to people with knowledge of the matter.” (Bloomberg)

“Blackstone Makes $2.29 Billion Deal for Japan Drug Business: Blackstone Group Inc. is buying the consumer health-care business of Japan’s Takeda Pharmaceutical Co. for ¥242 billion ($2.29 billion), one of the larger private-equity acquisitions in a country where such deals are slowly expanding.” (WSJ)

“Platinum Equity in Talks to Buy HNA’s Ingram for $7 Billion: U.S. private equity firm Platinum Equity is in advanced talks to buy HNA Group Co.’s Ingram Micro Inc. in a deal that values the technology distributor at about $7 billion, including debt, according to people with knowledge of the matter.” (Bloomberg)

“Warburg, TPG Invest in $12 Billion Norwegian Software Firm Visma: Warburg Pincus and TPG agreed to invest in Norwegian software developer Visma, valuing the company at 110 billion krone ($12.2 billion) including debt in one of the European technology industry’s biggest deals this year.” (Bloomberg)

Venture Capital

“Warby Parker gets a $3 billion valuation: Eyeglass-selling startup Warby Parker has raised $245 million with investments from D1 Capital, Durable Capital Partners, T. Rowe Price, and Baillie Gifford.” (Fortune)

“Freenome secures $270M to boost its colorectal cancer blood test, expand trial nationwide: Freenome continues to draw strong financial support for its development work, with $270 million in new funds to push its cancer-detecting blood test through clinical trials and across the finish line at the FDA.” (Fierce Biotech)

“Chinese commercial launch startup iSpace raises $172 million: The private launch industry isn’t showing any signs of slowing down, and a new $172 million Series B round of funding for China commercial launch startup iSpace indicates it could be heating up internationally.” (TechCrunch)

“Synthego raises $100 million for AI-driven gene editing: Synthego, which is developing a machine learning-based approach to engineering genomes, today closed a $100 million funding round” (VentureBeat)

“RIA Intel: Venture Capital Gives Wealth Management Startups the Cold Shoulder: Venture capital firms are not as enthusiastic about wealth management startups, if the number of deals, and the amount of money they are willing to invest, are indications. But it might just be a break, not a breakup.” (RIA Intel)

M&A

“Aveva to buy US tech group OSIsoft in $5bn deal: Aveva has agreed to acquire OSIsoft, its SoftBank-backed US rival, in a $5bn takeover that is one of the largest deals struck by a UK technology company.” (FT)

“LA gets a big SAAS exit as Fastly nabs the Culver City-based Signal Sciences for $775M: Signal Sciences, the security monitoring and management company, is getting bought by Fastly, a provider of content delivery networking services, for $775 million.” (TechCrunch)

“Palo Alto Networks to buy digital forensics consulting firm for $265M: The ever acquisitive Palo Alto Networks announced its intent to acquire The Crypsis Group, an incident response, risk management and digital forensics consulting firm, for a crisp $265 million.” (TechCrunch)

“Cisco acquiring BabbleLabs to filter out the lawn mower screeching during your video conference: Cisco, which owns the WebEx video conferencing service wants to do something about that, and late yesterday it announced it was going to acquire BabbleLabs, a startup that can help filter out background noise.” (TechCrunch)

IPOs

“Asana, Snowflake lead tech company rush to public markets in landmark day: A slew of Bay Area software companies with multibillion-dollar valuations filed for public listings on Monday, adding to a recent rush in a sign that markets are welcoming aspiring public companies with open arms.” (PitchBook)

“Palantir files to go public: Palantir, the secretive data analysis software company known for working with governments, has filed to go public via a direct listing on the New York Stock Exchange.” (Axios)

“Bitcoin Investor Files For Giant $350 Million IPO For Possible Merger: The founder of early bitcoin venture capital firm Ribbit Capital has filed for a massive $350 million initial public offering.” (Forbes)

“3D Printing Unicorn Desktop Metal To Go Public In Latest Deal With A Blank Check Company: 3D printing unicorn Desktop Metal is the latest company to go public in a deal with a blank check company. Expected valuation: Up to $2.5 billion.” (Forbes)

For those wondering how these Tweets are collected: There is no process. It’s just me. Scrolling through Twitter. Selecting the ones I like. Enjoy.

John Hyatt, author of What’s the Deal, is a financial writer and a Marjorie Deane fellow at NYU’s Arthur L. Carter Journalism Institute. Follow him on Twitter, connect with him on LinkedIn, email him your feedback at johngilberthyatt@gmail.com – and don’t forget to subscribe!